The courts and the commissioner have interpret §83(a), but you seemed to have your own interpretation agent. Would you mind sharing?

26 U.S. Code Chapter 1, Subchapter B - Computation of Taxable Income

PART II—ITEMS SPECIFICALLY INCLUDED IN GROSS INCOME (§§ 71–90)

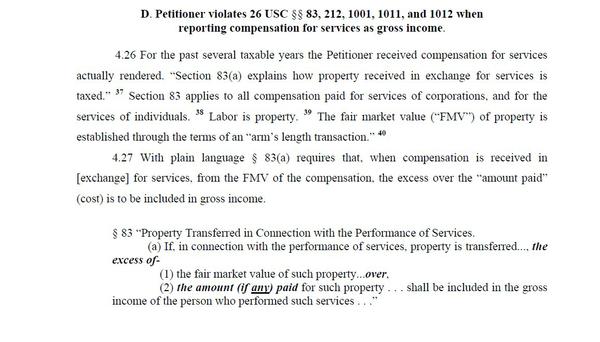

§ 83. Property transferred in connection with performance of services

(a) General rule

If, in connection with the performance of services, property is transferred to any person other than the person for whom such services are performed, the excess of—

(1) the fair market value of such property (determined without regard to any restriction other than a restriction which by its terms will never lapse) at the first time the rights of the person having the beneficial interest in such property are transferable or are not subject

to a substantial risk of forfeiture, whichever occurs earlier, over

(2) the amount (if any) paid for such property, shall be included in the gross income of the person who performed such services in the first taxable year in which the rights of the person having the beneficial interest in such property are transferable or are not subject to a

substantial risk of forfeiture, whichever is applicable. The preceding sentence shall not apply if such person sells or otherwise disposes of such property in an arm’s length transaction before his rights in such property become transferable or not subject to a substantial risk of forfeiture.

Now, to put it all into prospective now read:

If, in connection with the performance of services1, property2 is transferred to any person other than the person for whom such services are performed, the excess3 of … the fair market value of such property … over … the amount (if any) paid for such property,

shall be included in the gross income4 of the person who performed such services…

Simplified

- Services is labor; can you offer service without labor

- Labor/Services is property; if not, who owns your labor?

- Here is the definition of income “profit and gain”

- Gross income is taxable income