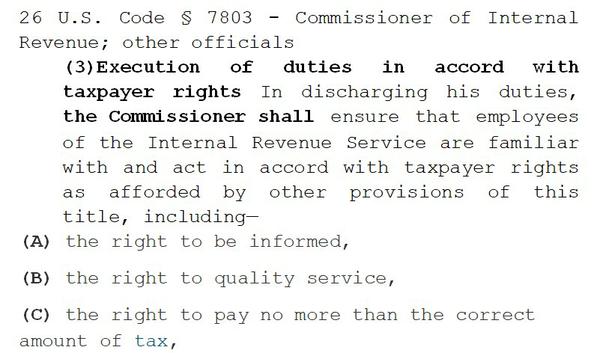

Well, US Tax Court knows full well what to do when confronted with a controversy under 26 USC § 83 -

“We shall begin our analysis with an exegesis [careful interpretation] of the general provisions of section 83. We then shall examine those provisions in conjunction with the facts of the instant case so that we may decide whether respondent adequately notified petitioner of the issue of the applicability of section 83. Section 83(a) generally provides that where property is transferred in connection with the performance of past,

present, or future services, the excess of the fair market value of the property over the amount paid for the property is includable as compensation in the gross income of the taxpayer who performed the services. Bagley v. Commissioner, 85 T.C. 663, 669 (1985), affd. per curiam 806 F.2d 169 (8th Cir. 1986). Section 83 does not apply only to

employees of the transferor of the property; rather, it is applicable to any person other than the one for whom the services were performed, including independent contractors of the transferor. Cohn v. Commissioner, 73 T.C. 443, 446 (1979). (footnote omitted). Thus, even though petitioner’s relationship to Immuno was that of an independent contractor rather than an employee, section 83 may apply to the receipt or disposition of the warrant by petitioner if the other

requirements of that section are met.”

See Pagel, Inc. v. Commissioner, 91 TC 200, 204-05 (Tax Court #34122-85, 1988).

HOWEVER, since 1993 when David R. Myrland began challenging the IRS claiming that it violates § 83(a) when the fair market value of personal

services are taxed as profit or ‘gross income’ the US government at every level flatly refuses to even mention the language of this governing provision or its implementing regulations.

The law says “any” is all inclusive, so cost would include personal services if the law says “any property” is a cost; right? Well, the law does indeed say that “any

money or property paid” for your compensation is a cost.

https://www.youtube.com/channel/UC4OSWo_uoplVCnphB-l4LPA/videos?disable_polymer=1

TalkShoe.com/tc/87488

WEvGOV.com